Home /

Expert Answers /

Advanced Math /

q1-let-varepsilon-t-be-an-i-i-d-process-with-e-left-varepsilon-t-right-0-and-pa668

(Solved): Q1 Let \( \varepsilon_{t} \) be an i.i.d. process with \( E\left(\varepsilon_{t}\right)=0 \) and \ ...

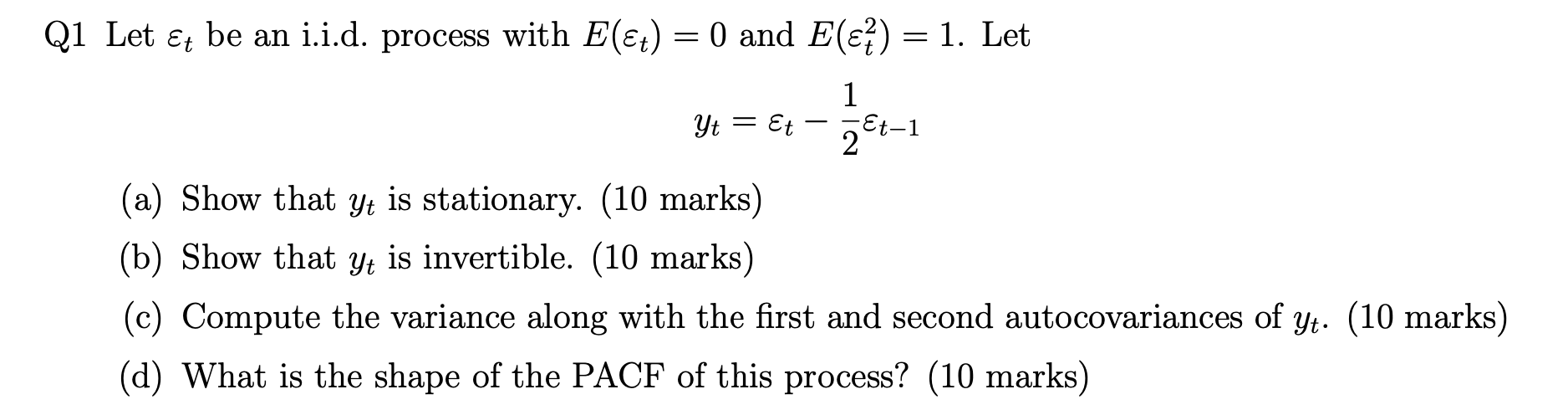

Q1 Let \( \varepsilon_{t} \) be an i.i.d. process with \( E\left(\varepsilon_{t}\right)=0 \) and \( E\left(\varepsilon_{t}^{2}\right)=1 \). Let \[ y_{t}=\varepsilon_{t}-\frac{1}{2} \varepsilon_{t-1} \] (a) Show that \( y_{t} \) is stationary. (10 marks) (b) Show that \( y_{t} \) is invertible. (10 marks) (c) Compute the variance along with the first and second autocovariances of \( y_{t} \). (10 marks) (d) What is the shape of the PACF of this process? (10 marks)