(Solved): The concepts of materiality and pervasiveness are important to audit teams in examinations of financ ...

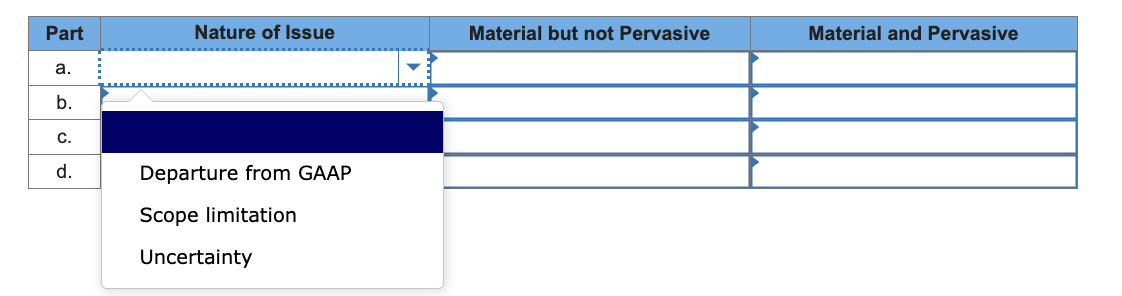

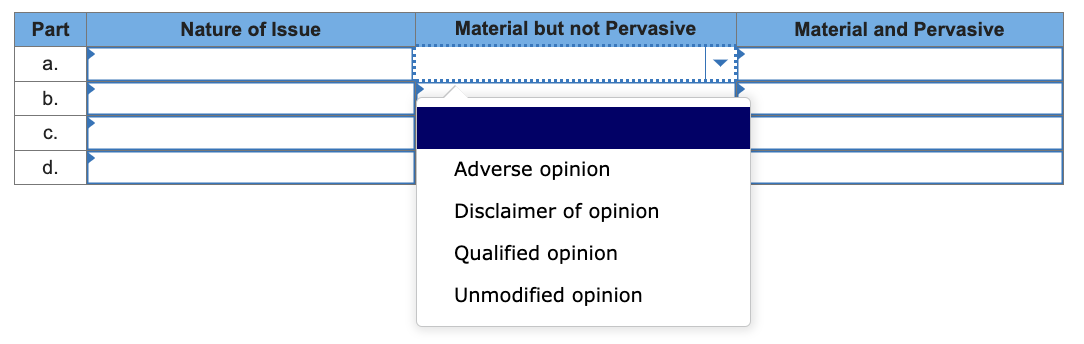

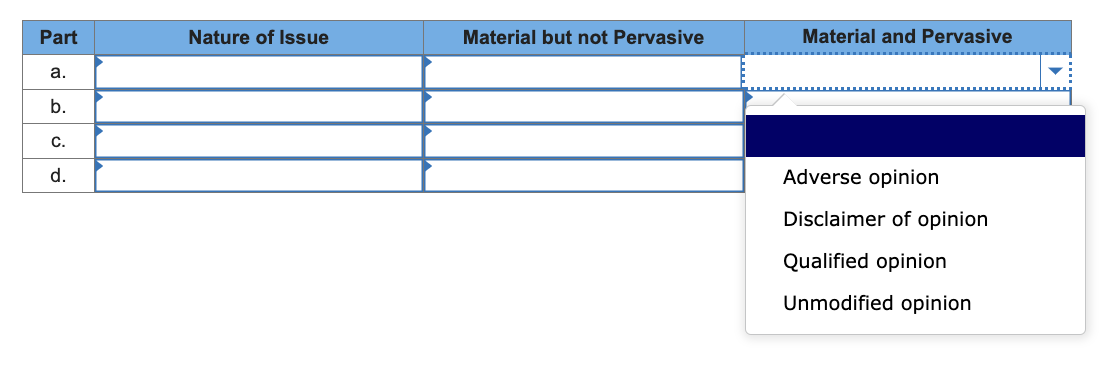

The concepts of materiality and pervasiveness are important to audit teams in examinations of financial statements and expressions of opinion on these statements. Required: Consider how the materiality and pervasiveness of each issue below affect the opinion expressed. For each issue you should identify the nature of the issue, the appropriate opinion if the issue is material but not pervasive, and the appropriate opinion if the issue is material and pervasive. a. The entity prohibits confirmation of accounts receivable, and sufficient and appropriate evidence cannot be obtained using alternative procedures. b. The entity is a gas and electric utility company that follows the practice of recognizing revenue when it is billed to customers. At the end of the year, amounts earned but not yet billed are not recorded in the accounts or reported in the financial statements. c. The entity leases buildings for its chain of transmission repair shops, but does not account for these lease obligations in accordance with GAAP. d. The entity has lost a lawsuit in federal district court. The case is on appeal in an attempt to reduce the amount of damages awarded to the plaintiffs. No loss amount is recorded. Scope limitation Uncertainty Disclaimer of opinion Qualified opinion Unmodified opinion