Home /

Expert Answers /

Statistics and Probability /

the-sample-covariance-between-the-random-variables-x-and-y-is-n1i-1n-pa529

???????

???????Expert Answer

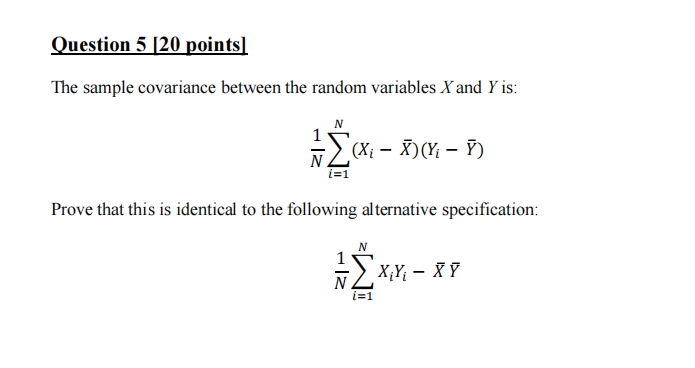

Let N be the number of observations, X_i be the value of the random variable X for the i-th observ