Home /

Expert Answers /

Accounting /

what-are-the-calculations-for-these-answers-with-the-red-flags-i-don-39-t-understand-how-these-are-c-pa775

(Solved): What are the calculations for these answers with the red flags? I don't understand how these are co ...

What are the calculations for these answers with the red flags? I don't understand how these are correct.

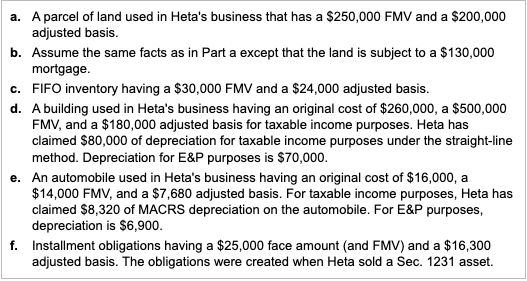

During the current year, Heta Corporation distributes the assets listed below to its sole shareholder, Donna. (Click the icon to view the list of distributed assets.) Assume that Heta has an E&P balance exceeding the amount distributed and is subject to a 21% tax rate. Unless stated otherwise, adjusted bases for taxable income and E&P purposes are the same.

a. A parcel of land used in Heta's business that has a $250,000 FMV and a $200,000 adjusted basis. b. Assume the same facts as in Part a except that the land is subject to a $130,000 mortgage. c. FIFO inventory having a $30,000 FMV and a $24,000 adjusted basis. d. A building used in Heta's business having an original cost of $260,000, a $500,000 FMV, and a $180,000 adjusted basis for taxable income purposes. Heta has claimed $80,000 of depreciation for taxable income purposes under the straight-line method. Depreciation for E&P purposes is $70,000. e. An automobile used in Heta's business having an original cost of $16,000, a $14,000 FMV, and a $7,680 adjusted basis. For taxable income purposes, Heta has claimed $8,320 of MACRS depreciation on the automobile. For E&P purposes, depreciation is $6,900. f. Installment obligations having a $25,000 face amount (and FMV) and a $16,300 adjusted basis. The obligations were created when Heta sold a Sec. 1231 asset.

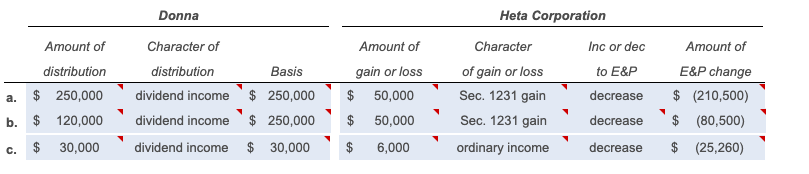

Amount of distribution a. $ 250,000 b. $ 120,000 30,000 C. Donna Character of distribution Basis dividend income $ 250,000 dividend income dividend income $ 30,000 Amount of gain or loss 50,000 50,000 6,000 $ 250,000 $ $ Heta Corporation Character of gain or loss Sec. 1231 gain Sec. 1231 gain ordinary income Inc or dec to E&P decrease decrease decrease Amount of E&P change $ (210,500) $ (80,500) (25,260)

Expert Answer

a. Heta recognizes $250,000 of dividend income and takes a $250,000 basis in the land. Donna Corporation recognizes a $50,000 Sec. 1231 gain. Donna’s E&P is increased by $50,000 and reduced by the land’s $250,000 FMV and by the $10,500 ($50,000 x 0.2